A Bird's Eye View

Why use a blockchain?

Key Takeaways

- •Traditional banking systems suffer from regulatory violations and conflicts of interest

- •DeFi provides stable coins, censorship resistance, and democratized access to financial services

- •The future of finance will likely blend traditional banking with DeFi innovations

The global financial system relies on intermediaries that process trillions in daily transactions, creating significant bottlenecks in worldwide capital movement. Technology has evolved, and the need for these institutions is diminishing, but they are still deeply ingrained in our society at an operational, regulatory, and influential level.

Some institutions have been deemed too big to fail, while others are allowed to collapse. Although these institutions are often reputable, they face ongoing scrutiny for opaque practices and frequent regulatory violations.

| Institution | Regulatory Fines | Violations | | --------------- | ---------------- | ---------- | | Bank of America | $82.7B | 214 | | JPMorgan Chase | $35.7B | 158 | | Citigroup | $25.4B | 122 | | Wells Fargo | $21.3B | 181 | | Deutsche Bank | $18.1B | 59 | | UBS | $16.7B | 83 | | Goldman Sachs | $16.3B | 44 |

These regulatory violations demonstrate systemic issues in traditional banking that have driven interest in alternative financial systems. Institutional failures and oversight account for some violations, but many result from individual misconduct and inherent conflicts of interest.

The revolving door between Wall Street and regulators exemplifies these conflicts. Former SEC Chairman Gary Gensler's background at Goldman Sachs and current Federal Reserve Chairman Powell's successful investment banking career highlight how regulators often emerge from the institutions they oversee. Since its inception, this fusion of private and public interests has been fundamental to America's financial system.

Central Banking

The Federal Reserve (FED) was established in 1913 as the third attempt at a central banking system in the United States. After the bank runs of 1907-1910, Chase Bank's founder, J.P. Morgan, and other influential bankers developed a plan that became the Federal Reserve—a hybrid faction within the US government that sets banking standards but operates independently of direct voter control.

The Mandate

The Federal Reserve operates under the "dual mandate," established by Congress in the Federal Reserve Reform Act of 1977.

The two primary objectives are:

- Maximum employment, which is not a specific unemployment rate.

- Price stability, which the Fed has interpreted as targeting 2% inflation over time.

The Fed seeks to achieve these goals through various monetary policy tools, primarily by adjusting interest rates and managing the money supply. The 2% inflation target wasn't officially adopted until 2012, when the Federal Open Market Committee (FOMC) explicitly stated this goal.

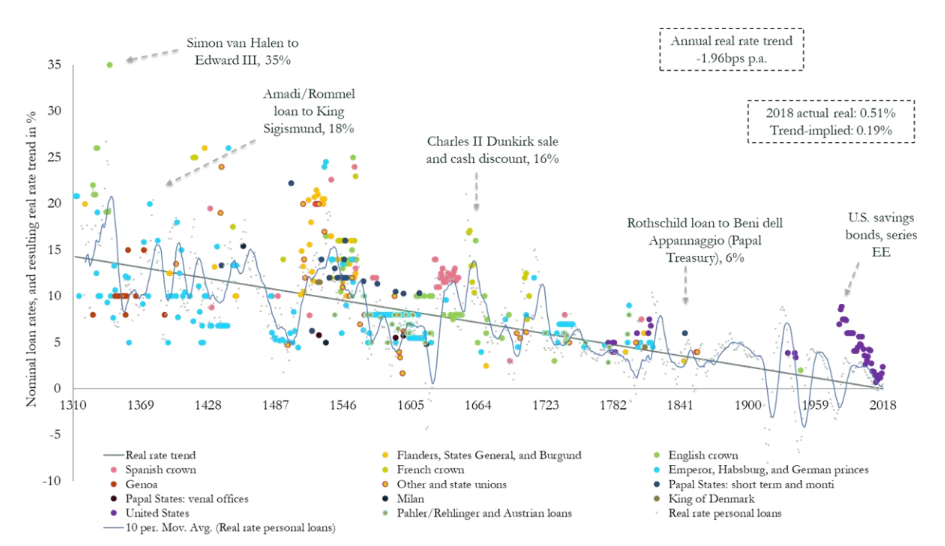

Although there are spikes, interest rates have been trending down for centuries.

Changing Value Perceptions

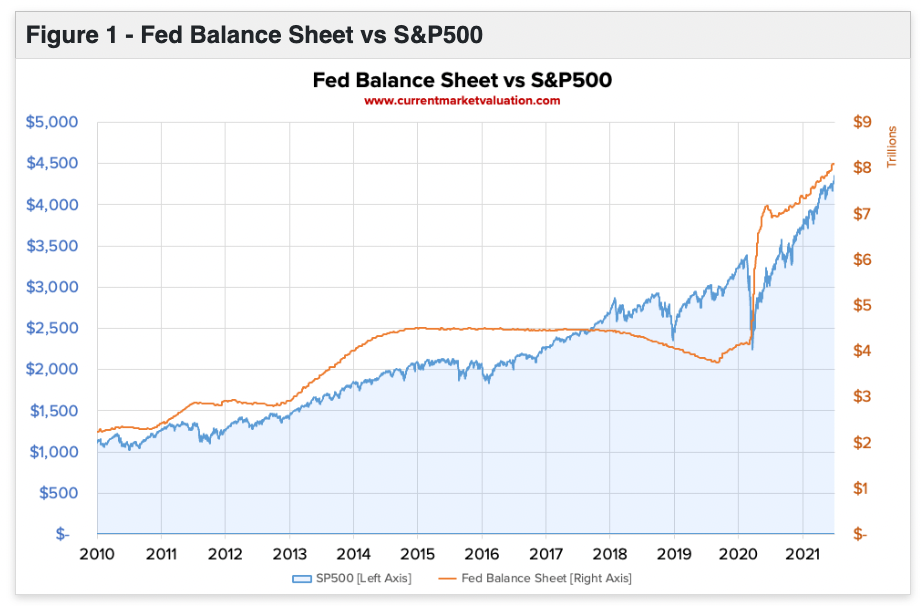

One way to evaluate the Federal Reserve's economic impact on value perception is through two key metrics: its balance sheet correlation with the S&P 500 and the US dollar's purchasing power trajectory. While correlation doesn't imply causation, monetarists who believe the printing of money directly affects the dollar's value have extensively studied these relationships. This has become particularly interesting following the Fed's interventions during the 2008 crisis and the COVID-19 pandemic.

Wall Street optimists argue that because of the US's dominance, it doesn't matter how much money is printed, and centralized intermediaries are a battle-tested system worth more than the trouble of occasionally bailing out a few bad actors.

In that world, where does Defi come in? It varies. If you're in one of the wealthier countries, you may utilize Defi as an alternative or speculative investment class. Still, those in less financially secure countries may be using Defi because they don't have any other option.

What's the alternative for those in non-financially secure countries? A continuation of opaque market procedures, unsustainable monetary policy, and hyper-inflationary events of debased fiat currencies becoming the norm?

Defi

Stable Coins

Let's consider Turkey as an example. The Turkish Lira experienced a reported 78% inflation from 2021 to 2022. While traditional, local banking systems offered limited recourse for such situations, digital, global alternatives now exist. Non-custodial wallets enable users to store digital assets securely without geographic restrictions or permission. These wallets are accessible through private keys or recovery phrases, allowing borderless value transfer.

Security considerations exist, but the practical benefits are clear: Moving any non-trivial amount of money across borders—especially in non-USD currencies—is extremely difficult through traditional banking. With Defi, it becomes trivial and can directly assist the needs of those in less financially secure countries today.

Censorship Resistance

In 2022, China's banking crisis revealed more risks of centralized banking controls. Four rural banks in Henan province froze $1.5 billion in deposits, affecting 400,000 customers. When depositors attempted to protest, authorities manipulated their COVID health codes from green to red, restricting their movement. By July, nearly 1 million customers were locked out of their funds.

Then, tanks were deployed against the protesters.

While China's response represents an extreme case of centralization and censorship, these issues exist on a spectrum worldwide—as does the need for Defi.

Yield Generation

Crypto builders have developed various approaches to generating yields with varying degrees of legitimacy and sustainability. Some mechanisms represent genuine financial innovation, but others - particularly centralized platforms like the now-defunct Celsius - have proved to be poorly regulated and over-leveraged systems that misrepresented risks. I met Alex Mashinsky, Celsius' CEO, a few months before the collapse, and he was dead-eyed. On the other hand, liquidity pools are an example of legitimate yield generation that democratizes access to trading profits.

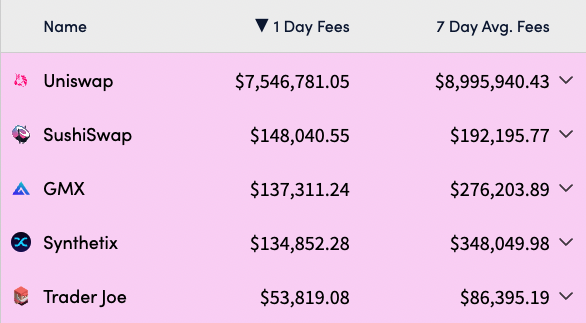

Unlike centralized platforms like Celsius, Automated Market Makers (AMMs) are smart contracts deployed on blockchains that enable asset trading through algorithmically managed liquidity pools—which is effectively what a DEX is. These systems compensate liquidity providers in two primary ways: through a share of trading fees or incentive token distributions.

Below are the top DEXes by 7-day average fees across various blockchains:

This democratization of market-making represents a significant shift from traditional financial structures. The blockchain infrastructure underlying these systems also brings unprecedented transparency, as trading activities and settlements are recorded on public ledgers, simplifying what was historically an opaque process.

Ryan Selkis, the CEO of Messari, recently published a thread of 35 use cases for which you can use Defi. It's worth a scroll.

A Balanced Approach

The emergence of Defi represents more than just a technological evolution in financial services—it marks a fundamental shift in how we think about and interact with money. Traditional financial systems have been the backbone of global commerce for centuries, but their limitations have become increasingly apparent in the digital age. Defi's promise lies in providing solutions addressing core limitations: accessibility, transparency, and censorship resistance.

The future of finance likely lies in the thoughtful integration of traditional and Defi systems, each serving its optimal purpose. Defi offers battle-tested, practical solutions today for those seeking alternatives—whether due to economic instability, political censorship, or a desire for financial autonomy.

Relevant Perspectives

Dr. Fabian Schär, Professor of DLT at the University of Basel:

"Defi protocols represent a paradigm shift in financial infrastructure, offering programmable and transparent alternatives to traditional financial services."

Gary Gensler, Former SEC Chairman:

"While Defi platforms may offer promising technological innovations, they still need to operate within a framework that protects investors and maintains market integrity."

Vitalik Buterin, Ethereum Co-founder:

"The goal of Defi isn't to oppose traditional finance, but to create an open, accessible financial system that complements existing infrastructure."

Advantages of Defi

Defi's advantages stem from its permissionless blockchain architecture. It offers unprecedented transparency through public ledgers for transaction and code auditing. Operating 24/7 with global accessibility removes traditional banking barriers of time zones and geography, providing anyone with internet access with the tools for financial autonomy, regardless of location or status.

Smart contracts automate complex financial operations without intermediaries, reducing costs and eliminating human error. This enables rapid innovation and the creation of novel financial instruments, which are impossible in traditional systems. Removing intermediaries also accelerates settlements from days to seconds or less.

Future Implications

Regulatory frameworks are developing at different speeds globally. While the UAE and Singapore foster innovation, others remain cautious. Europe's MiCA framework and US securities law developments will likely set important precedents.

The integration between traditional systems and Defi protocols is accelerating through stablecoins, CBDCs, and hybrid financial products. Success lies in leveraging both systems' strengths to build a more inclusive, efficient, and resilient financial infrastructure.