crypto · published

Unbanked to Bankless

How non-custodial wallets enable financial independence for the world's unbanked and underbanked populations.

Most people worldwide have at least one bank account, but over a billion adults don't.

Being unbanked or underbanked can be very destabilizing because you have to safeguard or carry your assets with you at all times and pay for everything in cash.

As blockchain technology has developed, anyone can generate a non-custodial wallet, which can serve as a decentralized bank and an investment account.

This removes the need to trust an intermediary to safeguard and give you access to your funds.

In its current form, it's not for everyone, but it's becoming a necessity for many.

No one can close your blockchain account, and no one can access your funds other than you.

You are nearly bankless, but you do need to configure on-boarding and off-boarding methods, which may require a bank.

While a covetable aspect of a developed society, banking has its issues.

This article breaks a few of them down and gets into the problems of being unbanked and the promise of going bankless.

The Unbanked

Definitions first, since the terms get blurred: the unbanked have no account at a bank or mobile-money provider at all; the underbanked have an account but still rely on alternative services like money orders, check cashing, or payday loans. The World Bank's Global Findex counted 1.7 billion unbanked adults worldwide in 2017; its 2021 update, published just before this article, lowered that to roughly 1.4 billion.

The share of unbanked citizens varies globally, from roughly 0% in countries like Norway and Sweden to over 70% in Morocco. Reasons also vary, but some causes are a lack of trustworthiness in domestic banking institutions and excess poverty.

Financially stable countries are generally more banked; however, in the US, the "richest" country globally, the Federal Reserve's 2019 wellbeing report classified 22% of adults - roughly 63 million people - as unbanked or underbanked.

Anyone who is unbanked is not able to partake in earning interest on deposits, investing in the stock market, paying bills online, purchasing goods or services over the internet, accessing credit, or several other valuable financial activities. There is also the need to use alternative financial services like money orders and prepaid cards, which are inefficient and rack up fees.

According to Forbes, "unbanked and underbanked Americans spent $189 billion in fees and interest on financial products in 2018".

While banking isn't a perfect system, using a good one undoubtedly gives an individual more financial freedom and ability than being unbanked.

The problem is that not all banks are good ones.

Issues with Banking

- Trustworthiness

Trustworthy bank accounts are a luxury in many parts of the world. In the US, most bank accounts are FDIC-insured for up to $250,000: deposit $250,000 into an FDIC-insured account and your money is backed by the full faith and credit of the US government, its military, and its money printer.

Non-US bank accounts are generally trustworthy, although developing countries with their currencies often experience volatility in purchasing power.

This, along with internal political and external geopolitical pressures, can result in what's known as a bank run, where everybody tries to withdraw their money at or around the same time.

Banks do not hold everyone's money simultaneously - they lend most of it out with interest to make money on your money.

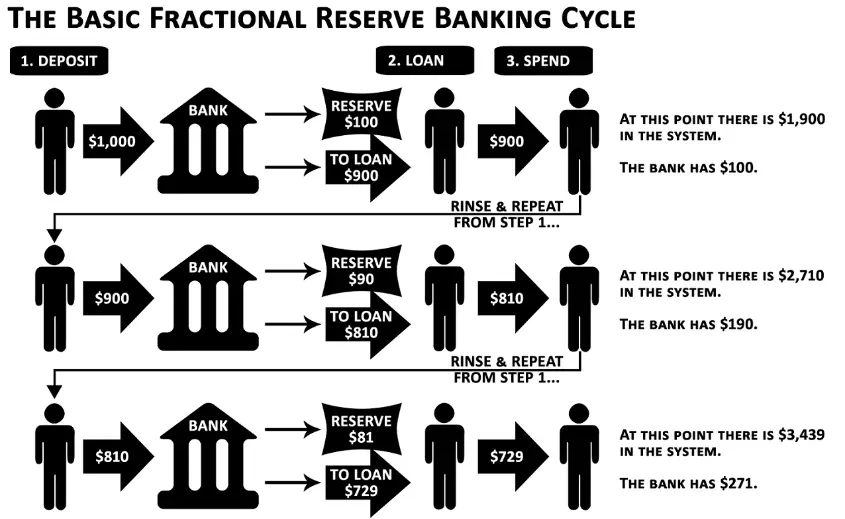

Fractional Reserve Lending

The textbook version: if the reserve ratio is 10%, a bank that takes your $10 deposit keeps $1 on hand and lends $9 to a borrower. That $9 gets spent, lands as a deposit at another bank, which keeps 90 cents and lends $8.10 - and so on across the system. Your $10 claim never went away, yet new spendable money now exists alongside it. That simultaneity is how bank lending expands the money supply, and it's also why every claim cannot be honored at once.

Two corrections to the folk version of this story: the expansion happens across the banking system through re-deposits, not because one bank "uses your money twice"; and modern banks aren't literally constrained by a reserve ratio at all - they create deposits when they lend and are limited by capital and liquidity requirements. The US cut its formal reserve requirement to zero in March 2020. The mismatch the textbook model illustrates, though, is real.

The theory behind fractional reserve lending is that capital creation drives economies forward.

Is it the real invisible hand?

Systemic Risk

When economies are riding high, fractional reserve lending is a bank's superpower, just as leverage is to your typical trader. Problems start appearing once currencies lose their value, and too many people try to withdraw their cash simultaneously. Your deposits are the funding base for banks to issue loans.

These loans are made with your liquidity, but you are not the one being rewarded for it – the bank is.

When you take out a loan, you borrow another depositor's liquidity.

US Treasuries invite a related, if imperfect, comparison.

Skeptics often refer to cryptocurrencies as Ponzi schemes, and in some cases, they are correct - though the same skeptics rarely examine how sovereign debt rollover works.

The US government spends more than its tax revenue and issues Treasury bills, notes, and bonds to fund the difference. These are IOUs paid back with interest, at what's called the risk-free rate - a name that flatters the arrangement. Maturing Treasuries are paid off with tax revenue or, usually, by issuing new debt.

The SEC defines a Ponzi scheme as investment fraud that pays existing investors with funds collected from new investors, and the surface mechanics rhyme: old obligations are serviced partly by new issuance.

The differences are what keep the comparison honest: Treasury borrowing is fully disclosed, backed by the state's power to tax (and, for a currency issuer, to print), and no investor is deceived about the structure. Rolling debt is not fraud. It is, however, a system that depends on continued confidence - which is the part worth remembering.

Bad Behavior

Aside from the global financial meltdown in 2008, which was caused by Wall Street and the banking system, banks have accumulated hundreds of billions of dollars in fines for other bad behavior.

Cumulative fines paid since 2000, per Good Jobs First's Violation Tracker as of this article's writing (late 2022):

Bank of America (US) – $82,737,699,939 over 214 fines. JPMorgan Chase (US) – $35,744,240,670 over 158 fines Citigroup (US) – $25,450,155,764 over 122 fines Wells Fargo (US) – $21,340,036,745 over 181 fines Deutsche Bank (Germany) – $18,156,533,878 over 59 fines UBS (Switzerland) – $16,792,800,910 over 83 fines Goldman Sachs (US) – $16,365,468,987 over 44 fines

Financial services are among the most fined industries in the world: over $330 billion across more than 6,000 fines since 2000, per the same tracker.

Going Bankless

As you can see, banking has its issues. Before Bitcoin and non-custodial wallets, the only way to be your bank was to be unbanked, and as detailed earlier, that also had its problems.

Bitcoin, then Ethereum, and thousands of other cryptocurrencies enabled anyone anywhere to open a private bank and investment account on a blockchain without requiring the trust of any third party.

It's counterintuitive, but you don't want to trust anyone regarding financial services. An ideal blockchain would not require participants to trust each other but rather serve as an operating system for applications to operate trustless and permissionless.

What are Non-Custodial Wallets?

Non-custodial wallets are immutable sources of record for your savings / HODL account.

When you deposit money into any custodial account like a bank or centralized exchange, you trust this counterparty to honor your balance and access your funds.

You don't have to trust any counterparty when using a non-custodial wallet.

The blockchain collectively verifies your balance, and only those with the mnemonic can access a wallet.

This is why it's so important to understand and safeguard your mnemonic phrase!

For more details, see Solflare's guide on mnemonic phrases.

The Honest Trade

Going bankless swaps banking's problems for crypto's, and the second list is not short: volatile assets (stablecoins help, but carry issuer risk), network fees that can spike, scams and phishing that target newcomers hardest, the burden of custody falling entirely on you, patchy internet and smartphone access in exactly the places that are most unbanked, uncertain regulation, and the persistent difficulty of converting crypto back into local cash. Whether the trade is worth it depends on how badly the local banking option is failing.

Conclusion

For the first time in history, individuals can self-custody their assets. Since so many people are still unbanked and the banking system has many problems, some are jumping straight from unbanked to bankless.

This phenomenon is most visible in parts of Africa and Southeast Asia, where unbanked rates are high and blockchain adoption surveys rank those regions near the top.

How far it goes will depend on the barriers above falling - cheaper fees, better off-ramps, safer wallets - not on the promise alone.