finance · published

Digital Gold

Bitcoin is more mimetic than gold

Bitcoin issuance per block

FigureBitcoin was initially intended to be a peer-to-peer medium of exchange1, although its narrative has shifted toward that of a global store of value.

As of early 2025, few of Bitcoin's prominent institutional advocates still pitch it primarily as a transactional currency - a highly volatile asset is poorly suited for everyday payments - though Lightning proponents and the communities actually using BTC for payments and remittances are real exceptions to that generalization.

Two arguments run through this piece, and they deserve to be kept separate. The first is the familiar checklist: scarcity, portability, divisibility, verifiability. The second is the one this article actually exists for: gold's value is itself mostly mimetic - people want it because others want it - and Bitcoin competes with gold on precisely that terrain, not just on the checklist.

(A note on the charts: figures labeled through 2025 were re-rendered after the original January 6, 2025 publication.)

Inflation

Inflation is the rate at which the general price level of goods and services rises. Financial regulators employ various methodologies to measure inflation, and monetary policy uses inflation as a mechanism to manage debt obligations over time. This allows governments to repay debt with currency of diminished value compared to when borrowed, effectively transferring wealth from creditors to debtors. Over time, this leads to loss of purchasing power and increased nominal asset prices, primarily benefiting asset owners while impacting wage earners at the point of consumption.

Traditional financial systems have experienced persistent inflation for centuries. The US Dollar, the world's dominant reserve currency, has lost approximately 97% of its purchasing power since the Federal Reserve's establishment in 19132. To help individuals hedge against inflation, governments offer bonds that pay fixed rates of return. These returns have typically ranged between 2-4% annually over recent decades3.

Banks capitalize on the spread between rates paid to depositors on savings accounts and rates received from government bonds and lending activities4. At certain periods, while government bond yields exceeded 2%, major banks offered savings rates as low as 0.01%—a spread of nearly 200:1.

Stores of Value

Money serves three purposes: unit of account, store of value, and medium of exchange5. If currency cannot be used to purchase goods and services, it fails as money. If it loses significant value over a year, a day, or even an afternoon—as the German population experienced during the 1923 hyperinflation documented in When Money Died—it fails as money.

Rather than hold depreciating national currencies like the Turkish Lira or South African Rand and experience declining purchasing power, many individuals have adopted Bitcoin, USDT, or other cryptocurrencies that enable pseudonymous, secure value transfers and opportunities for capital appreciation. USD remains the dominant global reserve currency. All other currencies are priced against and dependent upon it. For national currencies, appreciation against USD generally indicates economic weakness, as it requires more local currency to purchase the same quantity of USD.

The Turkish Lira has lost most of its value since 2018:

Figure 1: Turkish Lira Devaluation vs USD, 2018-2025. The TRY/USD exchange rate demonstrates severe currency devaluation, with the lira losing over 80% of its value against the dollar during this period due to inflation and monetary policy challenges.

The South African Rand has experienced extreme volatility over the past decade:

Figure 2: South African Rand vs USD, 2014-2025. The ZAR/USD exchange rate exhibits sustained volatility and general depreciation trend, reflecting South Africa's economic challenges and commodity price dependencies.

Bitcoin holders have substantially outperformed holders of traditional currencies over the past decade. The famous "Bitcoin Pizza" transaction saw 10,000 BTC exchanged for two pizzas valued at approximately $25-30 on May 22, 2010, representing a price of roughly $0.0025-0.003 per BTC6. Bitcoin set an all-time high above $108,000 in mid-December 2024, weeks before this article's publication7.

Figure 3: Bitcoin Price in USD, 2010-2025. Bitcoin's price appreciation from less than $0.01 to over $100,000 represents one of the most dramatic asset price increases in financial history, accompanied by extreme volatility.

USD holders experienced significant purchasing power decline relative to Bitcoin over this period:

Figure 4: USD Purchasing Power vs Bitcoin, 2010-2025. Inverted perspective showing USD purchasing power collapse against Bitcoin. While Bitcoin appreciated, this chart reflects the opportunity cost of holding dollars rather than Bitcoin during this period.

Gold

Physical gold bars have historically outperformed most assets during periods of economic uncertainty. As a result, gold has become a safe-haven asset - the destination of flight-to-quality flows - in the portfolio allocation frameworks of institutional investors.

Capital flows from speculative investments to safe-haven assets do not occur automatically. They result from investor psychology influenced by mimetic desire—people valuing assets because others value them—often manifesting gradually before accelerating rapidly in a phenomenon known as mimetic contagion.

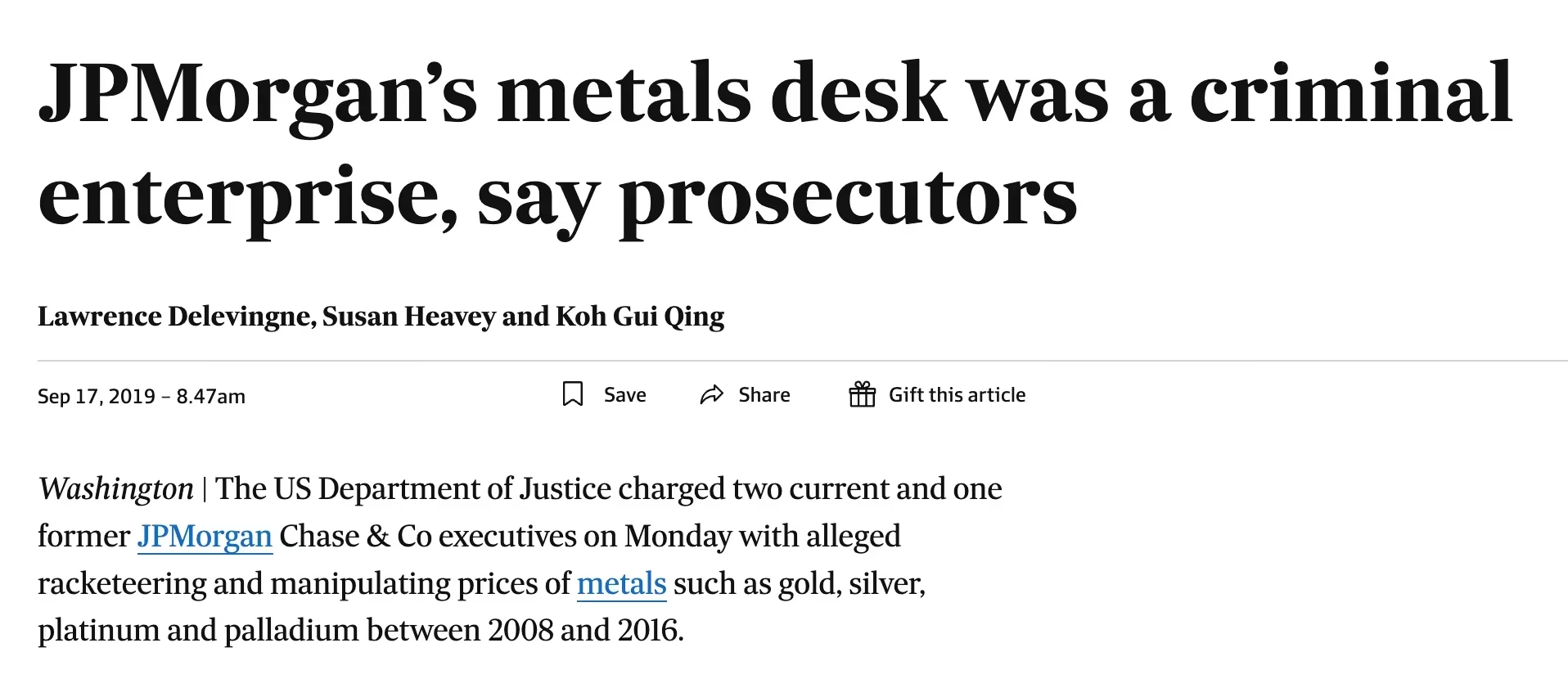

Beyond its use in jewelry and select manufacturing applications (electronics, aerospace), gold is perceived to exist outside traditional financial systems. However, central banks and financial institutions hold the largest gold reserves globally8. Gold derivatives markets are substantial, and price manipulation cases have resulted in significant regulatory enforcement actions9.

Figure 5: JPMorgan Gold Market Manipulation. JPMorgan Chase faced nearly $1 billion in fines for precious metals market manipulation, highlighting how even "safe haven" assets are subject to institutional price manipulation through derivative markets.

Digital Gold

Investors and media analysts have referred to Bitcoin as "digital gold," partly because this analogy provides the most accessible framework for understanding its market role and partly because the comparison has validity.

| Feature | Physical Gold | Bitcoin |

|---|---|---|

| Portability | Limited (heavy, physical) | Excellent (private keys enable global transfer) |

| Divisibility | Limited (physical constraints) | Highly divisible (to 8 decimal places: satoshis) |

| Verifiability | Requires testing (assay, purity tests) | Instant, certain (cryptographic verification) |

| Transfer | Slow, expensive (shipping, insurance) | Near-instant, global (blockchain settlement) |

| Storage | Physical (vaults, security required) | Digital (secured by cryptography) |

| Scarcity | Limited (finite earth deposits) | Fixed (21 million cap, programmatically enforced) |

Extrinsic Value and Mimetic Desire

While gold has performed well historically during economic distress, this appreciation stems from extrinsic rather than intrinsic value. Gold is difficult to transport or store at scale. The precious metals industry is highly concentrated among a relatively small number of institutional players. Gold's price fluctuates primarily based on extrinsic valuation—collective belief in its value rather than fundamental utility.

Mimetic desire, as theorized by René Girard, suggests people desire objects because others desire them. In asset markets, this manifests as investors purchasing gold not for its industrial utility but because other investors and institutions value it, creating self-reinforcing price dynamics.

Figure 6: Gold Price Chart, Long-term. Gold's price action demonstrates a classic cup and handle technical pattern, a formation suggesting continuation of the prior uptrend based on historical price behavior rather than fundamental value changes.

Counterarguments to Bitcoin's Scarcity

In its current state, Bitcoin should not serve as a primary transactional currency due to price volatility. Arguments for a decentralized global currency have theoretical merit, but the practical reality favors continued USD dominance for near-term transactions.

Prominent Bitcoin advocates like Michael Saylor (MicroStrategy CEO) project significant USD devaluation and potential hyperinflation scenarios10. Simultaneously, Saylor's company and institutional investors are accumulating substantial Bitcoin positions, concentrating ownership among corporate and Wall Street entities rather than distributing it broadly. This introduces new dynamics around ownership concentration and institutional influence.

Instead of serving as a payment mechanism, Bitcoin could function as a store of value due to its advantages over gold listed in the table above. Scarcity is a key component of both gold and Bitcoin's value proposition.

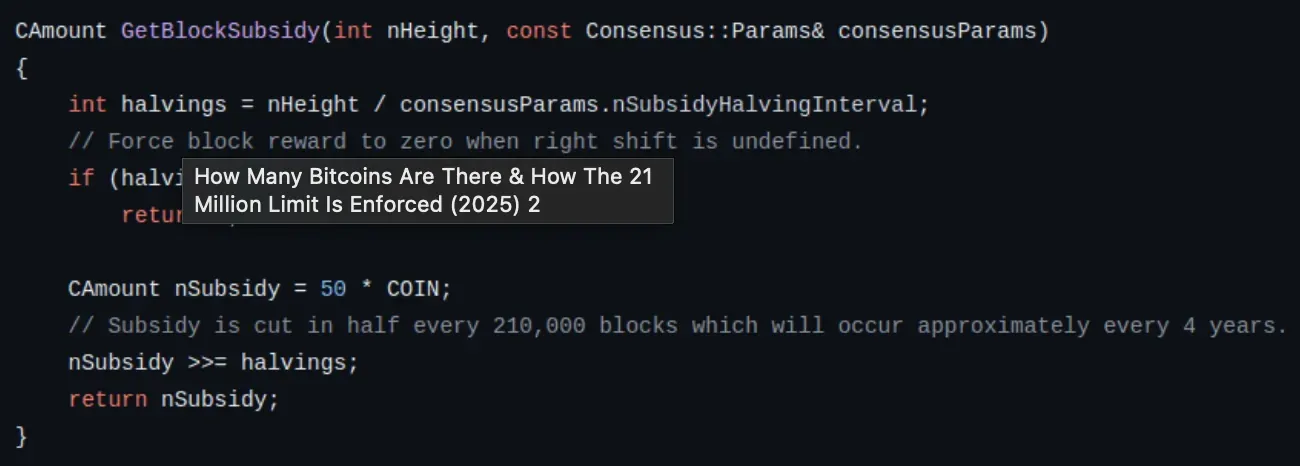

Gold's scarcity depends on geological factors (finite earth deposits), extraction economics (mining costs), physical properties (metal streaming), speculative future supply (asteroid mining)11, and institutional concentration. Bitcoin's scarcity depends on approximately 20 lines of code12:

Figure 7: Bitcoin Supply Cap Code. The Bitcoin protocol's supply cap is enforced through consensus rules in the software. This code limits total supply to 21 million BTC, with the final bitcoin scheduled for mining around 214013.

A small group of Bitcoin Core developers maintains the reference implementation software. Any protocol change requires consensus among this development community and, critically, adoption by the majority of network participants (miners, node operators, users). As of 2025, consensus rules define a maximum supply of 21 million BTC. Most of that supply already exists, with the final bitcoin scheduled for creation around 214013.

If all Bitcoin Core developers agreed to change the supply cap, a majority of computers on the network would still need to update their software and validate the new supply schedule. Bitcoin's verification process—proof-of-work mining—is an expensive undertaking. High capital and energy costs have resulted in a small number of mining pools controlling the majority of network hash power14.

While the 21 million cap theoretically could be changed, doing so contradicts the economic interests of developers, miners, and the network participants. Such a change would likely require a catastrophic event or fundamental shift in network incentives15.

However, Bitcoin faces several risks that potential investors should consider16:

Regulatory Risk: Government crackdowns, restrictions on exchanges, or outright bans could significantly impair accessibility and value.

Technological Vulnerabilities: While the Bitcoin protocol has held up under sixteen years of attack, quantum computing advances or undiscovered cryptographic vulnerabilities pose theoretical long-term risks.

Extreme Price Volatility: Bitcoin has experienced multiple 80%+ drawdowns, making it unsuitable for risk-averse investors or short time horizons.

Physical Security Threats: The $5 wrench attack represents a fundamental security concern where physical coercion bypasses cryptographic protections. High-profile attacks on cryptocurrency holders highlight real-world security challenges facing the industry.

Conclusion

Although gold has not served as a practical transactional currency for centuries, major financial institutions and portfolio managers recommend allocating 1-5% of investment portfolios to gold as a safe-haven asset17. Gold will store value until collective belief shifts and it doesn't.

If scarcity is the dominant argument for value, more scarce assets could replace gold if market narratives shifted. Bitcoin is one such candidate. Its fixed supply, superior portability, instant verifiability, and global transferability offer technological advantages over physical gold.

However, Bitcoin's volatility, regulatory uncertainty, and relative youth as an asset class distinguish it from millennia-old gold. Gold has 5,000+ years of cultural and institutional acceptance as a store of value. Bitcoin has 16 years.

Whether Bitcoin becomes "digital gold" depends on sustained network security, continued decentralization, favorable regulatory developments, and most importantly, sustained collective belief in its value—the same mimetic dynamics that have supported gold for thousands of years. Investors should carefully consider their risk tolerance and conduct thorough research before allocating significant portions of portfolios to any volatile asset, including Bitcoin.

Additional source links

- BLS CPI Inflation Calculator — $1 in 1913 has the purchasing power of roughly $30-33 in 2024 (~97% loss)

- FRED — Bank Net Interest Margin

- Bitcoin Pizza Day — the pizzas were valued at approximately $25-30 at the time

- World Gold Council — Gold Reserves — central banks and international organizations hold roughly 35,000 tonnes

- DOJ press release on the JPMorgan precious-metals settlement

- MicroStrategy Bitcoin strategy announcements

- Asteroid mining (overview) — the NASA/JPL feature linked in the original has been taken down

- Bitcoin Core GitHub repository

- Bitcoin halving schedule — the final satoshi arrives around 2140

- Ammous, Saifedean. The Bitcoin Standard (2018)

- Investopedia — Gold Portfolio Allocation — conservative advisors typically recommend 1-5%

Footnotes

-

Nakamoto, Satoshi. "Bitcoin: A Peer-to-Peer Electronic Cash System" (2008). ↩︎

-

Bureau of Labor Statistics CPI data, 1913-2024. ↩︎

-

Historical US Treasury yields available from US Department of the Treasury. ↩︎

-

Federal Reserve data on bank Net Interest Margin (NIM). ↩︎

-

For detailed analysis of money's functions, see Federal Reserve Education - Functions of Money. ↩︎

-

The famous "Bitcoin Pizza Day" transaction occurred on May 22, 2010, when Laszlo Hanyecz paid 10,000 BTC for two Papa John's pizzas. ↩︎

-

Bitcoin price data from major exchanges (Coinbase, Binance, Kraken). The mid-December 2024 all-time high printed above $108,000; exact figures vary slightly by exchange. ↩︎

-

World Gold Council data on official gold reserves. ↩︎

-

JPMorgan Chase paid nearly $1 billion in fines for precious metals market manipulation (2020). ↩︎

-

Michael Saylor has made numerous public statements projecting USD inflation and promoting Bitcoin as an inflation hedge. ↩︎

-

While asteroid mining remains speculative, some asteroids contain substantial precious metal deposits. ↩︎

-

The Bitcoin supply cap is implemented in the Bitcoin Core codebase through the block subsidy halving mechanism. ↩︎

-

Mining pool concentration data from Blockchain.com Pool Distribution. ↩︎

-

Changing Bitcoin's 21 million supply cap would require a contentious hard fork and would likely split the network. ↩︎

-

See Fidelity Digital Assets' published research on Bitcoin as an asset, and central-bank working papers on crypto-asset risk from the BIS and ECB. ↩︎

-

Traditional portfolio allocation frameworks (e.g., Ray Dalio's All Weather Portfolio) recommend 5-10% gold allocation. ↩︎