finance · published

A Bird's Eye View

A practical case for DeFi

The global financial system is built on a dense web of intermediaries that handle trillions of dollars in daily transactions.

While this architecture has historically supported worldwide trade and capital movement, it also creates bottlenecks, inefficiencies, and systemic risks.

Technology has evolved, but legacy institutions remain entrenched, not just operationally, but politically and socially.

Some are deemed too big to fail and others are quietly allowed to collapse.

Although many are reputable, their track records are marred by regulatory violations and unresolved conflicts of interest.

| Institution | Regulatory Fines | Violations |

|---|---|---|

| Bank of America | $87B | 214 |

| JPMorgan Chase | $40B | 282 |

| Citigroup | $25B | 122 |

| Wells Fargo | $27B | 181 |

| Deutsche Bank | $18B | 59 |

| UBS | $16B | 83 |

| Goldman Sachs | $16B | 44 |

Source: Violation Tracker database, cumulative fines and penalties since 2000, as retrieved for the 2022 version of this article. The tracker's totals grow as new penalties are added, so current figures will differ. The seven institutions above alone sum to roughly $229 billion.

These numbers suggest systemic issues beyond regulatory oversight - structural design flaws in how financial incentives and accountability are balanced.

To make matters worse, the lines between regulator and regulated are often blurry.

Gary Gensler - SEC chairman at the time of this writing - spent 18 years at Goldman Sachs, becoming one of the youngest partners in firm history, before overseeing Wall Street.

Fed Chair Jerome Powell was a partner at The Carlyle Group from 1997-2005, building wealth in private equity and investment banking before setting monetary policy.

Janet Yellen earned over $7 million in speaking fees in 2019-2020 from Wall Street firms including Citi, Goldman Sachs, and Credit Suisse - the very institutions she would later regulate as Treasury Secretary.

To be precise about what this shows: none of these career paths is evidence of wrongdoing, and deep industry expertise is arguably a prerequisite for the jobs. The documented facts are about proximity, not corruption. But proximity is exactly what makes accountability hard to referee - the so-called "revolving door" between Wall Street and Washington is not new; it's the norm.

Central Banking Mandates and Mechanics

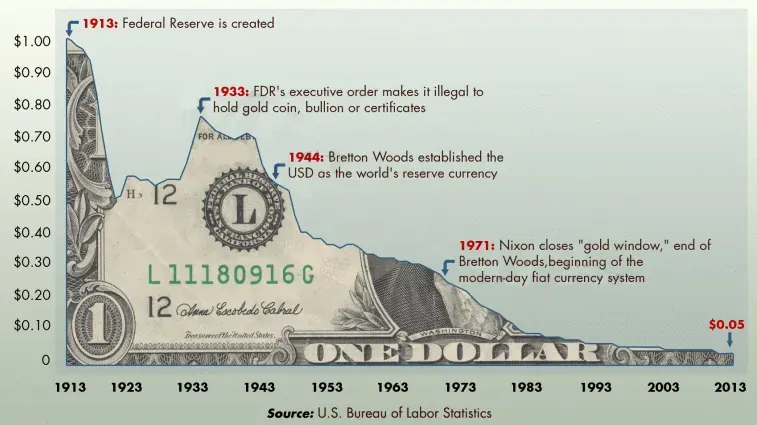

The Federal Reserve was formed in 1913 after a series of bank runs.

The plan was drafted at a secret meeting in November 1910 at Jekyll Island, where six men including J.P. Morgan's senior partner Henry Davison designed what would become the Federal Reserve System.

The Fed is a quasi-governmental institution: accountable to Congress in theory, but operationally independent in practice.

Its "dual mandate" was formalized in 1977 through the Federal Reserve Reform Act:

- Maximize employment

- Maintain price stability (interpreted as roughly 2% inflation since 2012)

While monetary policy has evolved, its tools have remained consistent: interest rate adjustments, balance sheet expansion, and open market operations.

Since January 2012, the Fed has explicitly targeted 2% annual inflation, and this goal has widespread implications for asset values and the purchasing power of the U.S. dollar.

Over the longer arc of history, interest rates have followed a steady downward trend.

As financial systems have become more sophisticated and interconnected, the cost of borrowing has decreased.

Value and Perception

Since 2008, the Fed's balance sheet and the S&P 500 have become increasingly correlated, raising questions about the long-term impact of monetary expansion.

The U.S. dollar's reserve currency status arguably provides more flexibility for monetary expansion than other nations possess, with global demand for dollars potentially buffering against inflationary pressures - but not every country enjoys that privilege.

In many parts of the world - particularly where goods and services are not denominated by major currencies like USD or EUR - DeFi isn't an alternative, it's a necessity.

While citizens in developed economies debate the theoretical benefits of decentralization, billions of people face immediate problems that traditional banking either can't or won't solve.

Currency devaluation, capital controls, lack of banking infrastructure, and political instability create daily financial challenges that demand solutions beyond the reach of conventional institutions.

Stablecoins and Inflation Hedges

Between 2021 and 2022, Turkey experienced severe economic turmoil with inflation reaching 78.62% year-over-year in June 2022 according to the Turkish Statistical Institute (TURKSTAT) - the highest rate in 24 years.

For citizens, local banks offered no effective recourse, but DeFi did. With stablecoins and non-custodial wallets, people could secure value, transact globally, and bypass unfair capital controls, all with open-source tools accessible to anyone.

These wallets required no bank account, no paperwork, just a private key or mnemonic phrase, which granted access to the on-chain accounts.

Censorship Resistance

In early 2022, Chinese authorities froze approximately $1.5 billion in customer deposits across four rural banks in Henan province.

When protestors gathered in July 2022, officials reportedly manipulated COVID health tracking systems to restrict travel and limit dissent. Over 1,000 depositors protested, and hundreds of thousands were locked out of their funds.

Chinese authorities later arrested 234 suspects allegedly involved in the banking scandal.

Centralized financial systems can restrict access to user funds based on policy decisions, while DeFi offers an alternative model: infrastructure built on open protocols and governed by code rather than regional authorities.

Yield and Innovation

DeFi protocols have introduced programmable implementations of financial primitives - lending, borrowing, trading, insurance, and more - though this innovation introduces new technical and economic risks.

The risk column of this ledger deserves its own honest accounting, especially in 2022: Terra's algorithmic stablecoin erased tens of billions of dollars in May; bridge hacks (Ronin, Wormhole) took nine-figure sums; "decentralized" governance often concentrates in a few large token holders; centralized stablecoin issuers can freeze funds; and the US sanctioning of Tornado Cash in August showed that enforcement reaches protocol-level infrastructure. Survivorship is doing real work in any optimistic DeFi narrative, this one included.

The survivors, like Automated Market Makers (AMMs) and liquidity pools, represent what DeFi does best: creating transparent, permissionless infrastructure that distributes trading fees to liquidity providers rather than concentrating market-making profits among gatekeepers.

This is a drastic departure from traditional finance, where market access, and especially market-making, is gated and opaque.

A Balanced Future

In the near term, the future of finance will likely be neither fully decentralized nor fully centralized, but rather a hybrid system.

DeFi is not a wholesale replacement for traditional finance, but it addresses specific gaps that legacy systems often ignore: accessibility, censorship resistance, and transparency.

In economies hampered by regional inflation or financial repression, DeFi is already solving practical, day-to-day problems.

In countries like the US, where banking systems are more secure, their value propositions are valid - but in practice, they become more theoretical.

For most people in stable economies, traditional banking offers superior convenience, consumer protections, and reliability that DeFi hasn't fully matched yet. Once legacy rails upgrade to use blockchains as their settlement layers, this theory will become more of a reality for everyone.

Until then, the space comprises individuals seeking financial sovereignty, founders building at the frontier, and sophisticated capital using DeFi primitives to earn higher risk-adjusted yields - alongside substantial speculative activity including meme tokens and airdrop farming.

Why DeFi Matters

In a world of economic volatility and institutional mistrust, decentralized systems are beginning to offer the ability to enhance legacy payment rails and financial operations using novel blockchain attributes.

DeFi’s architecture - permissionless, global, and transparent - unlocks new financial freedoms. It removes barriers of geography, status, and institutional gatekeeping. Smart contracts automate complexity, cut costs, and eliminate friction in ways legacy infrastructure simply can’t.

There are risks, but there's also progress.